25/03/2022

“What’s in a name? That which we call a rose, by any other name would smell as sweet”* … unless it’s a camellia, of course.

A key barrier to the adoption of responsible investing is the lack of consistency in both terminology and definitions

Research in Finance (RiF) has now completed its third annual UK Responsible Investing Study (UKRIS). Stage 1 of the study is an online survey. We are currently examining what the data reveals about the uptake of – and barriers to – the implementation of responsible investing (RI). A positive finding was that basic knowledge and understanding of RI improved again this wave, versus last year, with nearly half of the intermediaries taking part now able to name nine ESG issues, compared to two fifths a year ago and just a quarter of respondents two years ago.

What’s in a name indeed? While a rose and a camellia are both beautiful flowers, the vast majority of camellia varieties – and the ones deemed to have the best blooms – have no scent at all, as keen gardeners know.

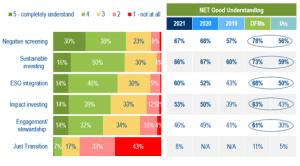

With respect to our survey, among the 215 DFMs and advisers who took part this year, we found that the lack of consistency in both RI terminology and definitions impedes understanding. We believe that there is still much to be done with respect to education, with around half of the participating intermediaries admitting a less than solid understanding of ‘impact investing’ and ‘engagement/stewardship’. We are still putting the finishing touches to the institutional component of the research (comprising the opinions of 151 pension schemes and consultants), where we are also seeing knowledge gaps in this market, for impact investing as well as other terminology.

Regarding intermediaries, in the chart below, when we asked how DFMs and IAs would rate their own knowledge and understanding of a number of RI terms, ‘Just Transition’ came out as the least understood term. In fact, only 11% of DFMs and 5% of IAs rated themselves as having a good understanding of this term.

There could be a number of reasons behind this. This is the first time that the relatively new term ‘Just Transition’ has been assessed in UKRIS. The way it is phrased could in itself potentially lead to misinterpretation. ‘Just Transition’ represents the initiative of the European Bank for Reconstruction and Development (EBRD) set out in June 2020. We at RiF referred to their definition with participants. The term ‘just’ in this instance means ‘equitable, fair’ rather than meaning ‘simply’ (as in ‘simply get on with the transition’). Trying to avoid confusion is key, as RI terms continue to originate from an increasing number of government and supra-national initiatives.

So what is ‘Just Transition’? In their own words, “The EBRD’s just transition initiative aims to help the bank’s regions share the benefits of a green economy transition and to protect vulnerable countries, regions and people from falling behind. The initiative builds on the EBRD’s experience of fostering transition towards sustainable, well-functioning market economies, and will focus in particular on the link between the green economy and economic inclusion. Working with national and regional authorities, EBRD clients and other partners, the initiative emphasises policy and commercial financing interventions that support a green transition while also assisting workers (particularly those whose livelihoods are linked to fossil fuels) in accessing new opportunities.”

UKRIS also revealed that CPD-accredited seminars remain the preferred means of training/support for both DFMs and IAs, with 64% interested in this. Intermediaries state that their preferred source of information to keep updated on RI is the asset managers that they work with. There may, therefore, be scope for asset managers to increase the descriptive content within the materials they provide, in order to define and refine RI terms in this fast-moving space. Meanwhile, the study identified that DFMs typically use their own firm as an RI resource (64%) compared to just 27% of IAs. It might be of interest to review how DFM firms create their materials and what inputs they themselves value the most from the sources they use, including asset managers’ materials.

Jack Dominy, Research Manager at RiF, summed up the findings: “Overall understanding and knowledge of responsible investing has undoubtedly improved in the last few years among retail intermediaries, as a result of increased media coverage on climate change and other ESG issues, as well as greater awareness in general from DFMs, IAs and their clients, as indicated by the findings from Wave 3 of the UK Responsible Investing Study. However, as the number of terms around RI and the resulting complexity of some of the terminology also increases, asset managers and the industry more broadly must find a way to ensure consistency and transparency as this is of paramount importance. Otherwise, there is a risk that there will be a ceiling on understanding, awareness and – ultimately – uptake with regards to responsible investing and solutions that are aimed at protecting the planet for the future.”

If you would like to know more about the UK Responsible Investing Study and how to subscribe, please contact Toby Finden-Crofts or Richard Ley. Options exist to purchase Wave 3 (fieldwork December 2021 to January 2022) or to become a full member with access to the online community for Wave 4 by expressing an interest now.

To discuss any points raised in this article please contact Catherine McNaught, Head of Content.

*“Romeo and Juliet”, Apologies to William Shakespeare.

Catherine is a highly skilled writer and editor with extensive experience working for B2B and B2C audiences, most recently at Schroders. Previous experience has included Standard Life, BlackRock, AXA Investment Managers and HSBC. A researcher and co-author of thought leadership materials and investment insights, she has a detailed knowledge of asset classes and investment themes including sustainability.