05/05/2020

As much of the world remains in varying degrees of lockdown, it’s hard to keep track of what the markets are doing on any particular day. We’ve seen share prices tumble, bounce, repeat and oil prices plumb negative territory.

Hopeful news of Covid-19 treatments and aborted drug trials continue to make for fitful markets.

One thing you can rely on during this time: lower dividend payouts. At last count, more than a third of FTSE100 companies had announced they would trim or completely scrap dividends, at least for the duration of the pandemic. Once trusty keystones of UK equity income strategies, banks and insurers are now holding back dividends, heeding advice from financial regulators to shore up their cash reserves and be ready for a potentially prolonged rough economic ride.

Income from property will also be hit by the pandemic, as temporarily-shuttered businesses struggle to make good on their rent and property funds themselves are suspended.

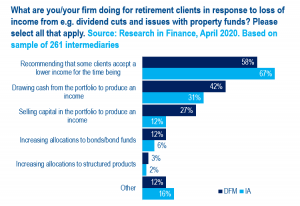

With this in mind, we felt it pertinent to ask DFMs and investment advisers (IAs) what this means for their retirement clients. Most intermediaries surveyed have suggested to some clients that they accept a lower income for now.

This finding makes sense – household spending has shrunk dramatically, so many full or semi-retirees can get by on less. Last month, the Office for National Statistics (ONS) released data showing a record-breaking 5.1% fall in retail sales volumes for March. Perhaps to be expected with spending on public transport, hospitality and lesiure activities decimated, and fashion brands also taking a hefty hit. But bear in mind that we were only in lockdown for half of March, and that some people were in full panic-buying mode. Keeping bellies (and the wine rack) full at home has meant higher sales for supermarkets, grocers and off-licences, but this doesn’t balance the falls in spending elsewhere. The Centre for Economics and Business Research estimates that average monthly household spending is down 30% and predicts higher monthly saving in Q2 overall, even when taking into account job losses, wage reductions and scaled-back hours for workers.

Another strategy intermediaries are adopting – DFMs especially – is drawing cash from the portfolio to produce an income. In the second half of last year, fear of fall-out from the US-China trade row and/or Brexit – or in some cases simply the feeling that markets were a bit ‘toppy’ – drove many firms to increase cash allocations. These would cushion the impact of future market blows and allow them to take advantage of more attractive valuations whenever these should arise.

The cash cushion also means that some DFMs and IAs can produce a regular income for retired clients without having to sell assets and crystallise losses (sometimes known in the trade as ‘pound-cost ravaging’), or at least minimising the extent to which they have to do this. One DFM told us, “A lot of clients already held sufficient cash to cover several years of income,” although over a quarter of DFMs report that they have actually been selling capital as well.

On this occasion, we didn’t ask intermediaries whether they will be allocating more to investment trusts to shore up income for clients; this is something we will be investigating through our ongoing UK Investment Trust Study. Dividend reserves mean that trusts are better positioned to continue paying out dividends, even when the underlying companies have put the brakes on their payouts. Some investment trusts have already announced they will not be breaking their respective dividend growth streaks: City of London will proudly preside over its 53rd consecutive year of dividend growth.

Our question on dealing with loss of income is of course a crucial one, and the answers tell us something about what intermediaries think is right, and what their clients can and are willing to accept, in extraordinary times. What the chart doesn’t speak to is the fact that recommendations on this issue are very personal – they will be different depending on individual circumstances. Can the client rely on a DB pension for the time being? Have they recently taken on a mortgage, buy-to-let or otherwise? What do their savings pots look like? Are they paying or contributing to uni fees?

At times like these, the value of personal advice and wealth management is so much more apparent than when everything is ticking up.

Annalise has spent her working life intensively researching B2B and B2C audiences in the financial sector. A keen qualitative researcher, she has conducted thousands of interviews across advisers, DFMs, fund houses, platforms, pension providers and consumers.