16/03/2023

As the 31st July 2023 deadline for implementation of the Financial Conduct Authority’s new Consumer Duty rules draws ever closer, tensions in the general insurance market are reaching new highs.

The market feels rather battered by new regulations, having had to cope with fair value assessments (FVAs) and the general insurance pricing review in the last few years. While some feel these have equipped the sector well for the arrival of the Consumer Duty, the FCA is not so convinced.

More than a tick box exercise…

Its most recent “Dear CEO” letter to the sector at the beginning of February was critical of firms taking a tick-box approach to FVAs, warning that carrying this approach over into the new regime will not be acceptable. This has left some, especially in the broking sector, unimpressed.

Sales, marketing, price and value are all key elements in the Consumer Duty but the FCA will also be looking at measuring value using claims data, especially when it comes to popular policy add-ons such as GAP insurance, legal expenses, uninsured loss recovery and some personal accident covers. These have been profitable areas for brokers but sometimes are not as well explained as the core product to which they are attached. When the expectations on communications are pulled into the mix, the industry is realising it still has a lot of work to do.

At the core of Consumer Duty is the principle of consumer outcomes and that has to be seen – and measured – from the customer’s perspective. Understanding what this means has left some firms behind. Research recently shared by the Association of British Insurers suggested that a third of people struggle to understand the terms and conditions of insurance products and services. Ultimately it is not about whether the insurer or broker believes their communications are clear: it is about how the customer understands them.

With the FCA reminding firms that they must communicate effectively at every stage of a policy’s lifetime “in a way that supports consumer understanding and equips consumers to make effective, timely and properly informed decisions”, many firms are now struggling to carry out a comprehensive review of their communications required to deliver this.

The issues highlighted in the FCA’s Dear CEO letter have underlined just how important the regulator sees Consumer Duty, the first fully fledged new principle it has introduced in 20 years.

How does the insurance industry view Consumer Duty?

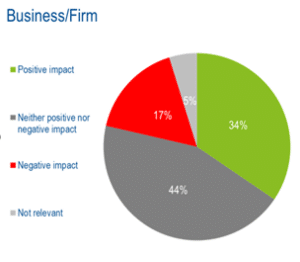

In a recent Research in Finance survey in which we questioned over 280 insurance professionals about their views on their preparations for Consumer Duty and how they expect it to impact their business and clients base. From the chart below you can see that 34% expect a positive impact.

What impact do you expect consumer duty regulation to have on your business?

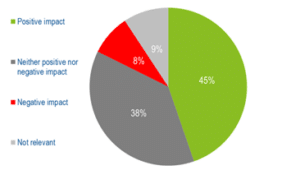

Conversely, it seems that 45% of those surveyed expect the new regulation to have a positive impact on their clients.

How do you expect the new consumer duty regulation will affect your clients?

It seems, then, that the industry recognises the advantages of the upcoming regulation. But how do they plan to prepare for it?

We asked the respondents to provide an example of some of the changes the insurance industry anticipates having to implement to meet the new consumer duty requirements and the main responses provided can be summarised as:

Key focus is clearly on reviewing clients’ needs, compliance requirements and collateral. Which is where we come in.

How can we help?

Here at Research in Finance we have already begun work with our clients supporting them as they work to meet the new regulation. We are working in collaboration to create an industry standard solution, giving them the security of knowing they are fully prepared for and complying with the consumer duty rules, as well as doing the best they can by their clients.

The rules need to be met within a short timeframe however it is not too late to ensure you are well prepared to meet the new regulation. We are here to support you as you plan and implement your response to the new Consumer Duty.

To find out more about how we can help with your Consumer Duty requirements, please get in touch with Mick Hrabe or Richard Ley. You can also call us on +44 (20) 7104 2235.

Karen is a very experienced insight manager having worked for more than 20 years client side across numerous industries undertaking market research projects (both qualitative and quantitative) as well as competitor and market intelligence. She has also facilitated many strategic workshops designed to tease out insights to inform company decision-making and product development plans. Karen joined Research in Finance recently from Canada Life where she was the Market Research and Insight Manager with responsibilities for research covering Equity Release, Protection, Retirement Income Planning and Wealth Management. Karen is a certified member of the Market Research Society.